MasterBrand (MBC) Deep Dive

A Value Play With Serious Torque to US Housing

(January, 2024)

Executive Summary

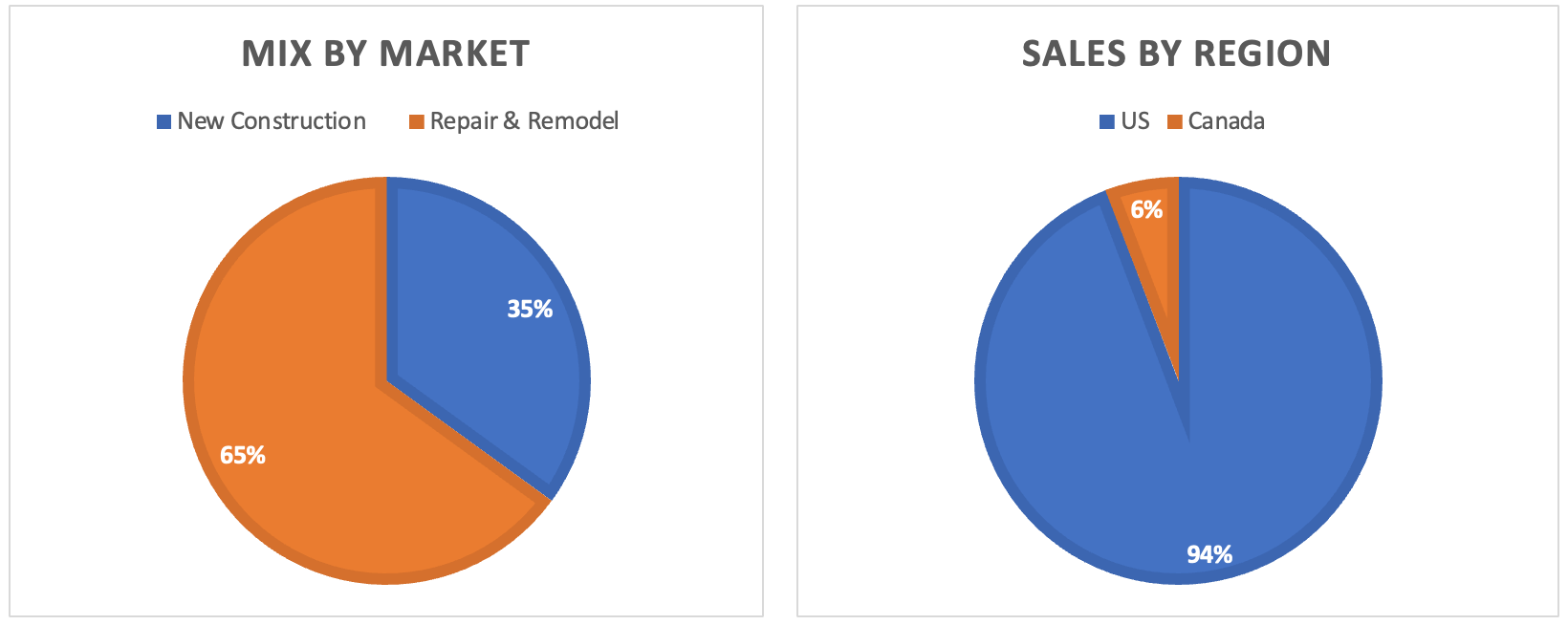

Masterbrand (MBC) is North America’s #1 manufacturer of kitchen cabinets with ~24% market share. The company caters to New Homes (35% Revenue) and Repair & Remodel (65%).

MasterBrand’s history is one of growth by M&A without any real integration. The new CEO is making tangible changes. Dave was a fighter pilot in the US Air Force and then cut his teeth at two of the nation’s greatest operators, Danaher and Roper. He is integrating the disparate collection of brands manufacturing on a single site into a series of multi-brand networks to increase utilization through the cycle. Dave is also converging platforms to generate efficiencies and economies of scale, reducing SKU count by over 70% across the portfolio. I will note, that many of these styles looked very similar to the consumer but may have been manufactured differently.

This is a market leader in a cyclical industry at the beginning of a multi-year upswing in US housing. Cabinets are a largely discretionary purchase, meaning both New Build and Repair & Remodel tend to move with the housing cycle. You will find my case for US housing in this report.

All you need to know for now is that MBC is a cheap stock with healthy torque to US housing. In a strong market with shrewd capital allocation, this stock could double in 3 years.

Company Overview

Masterbrand is North America’s #1 residential cabinet manufacturer with products sold throughout the US and Canada catering to the Remodelling and New Construction markets.

They operate primarily in the US, but Canada makes up ~6% of sales. Repair and Remodel are a larger portion of the mix but there is still a healthy weight to New Construction.

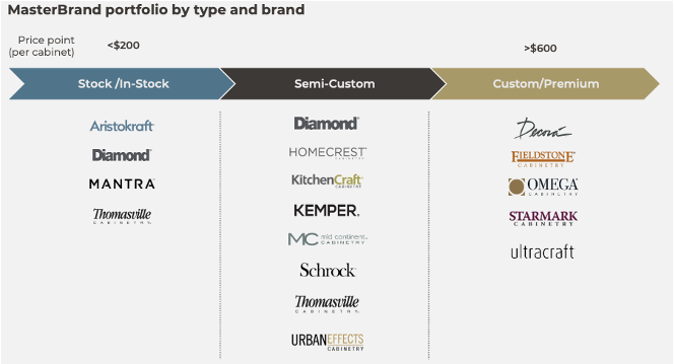

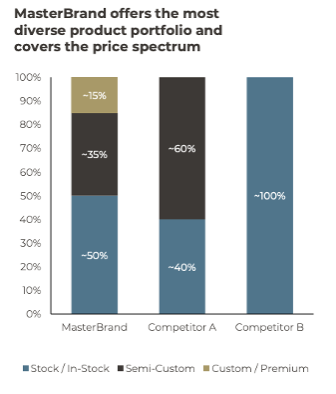

They operate under 16 brands with products catering to all price points;

· Stock Products (sub-$200) - Value-focused with low design complexity, standardized components, and shorter lead times.

· Semi-custom ($200 - $599) – More styles and features than stock cabinets.

· Premium (over-$600) – Highly customizable cabinets to meet their exact specifications.

I implore you to check out the products on their website: MBC Cabinet Brands and watch this short YouTube video; MasterBrand Introduction.

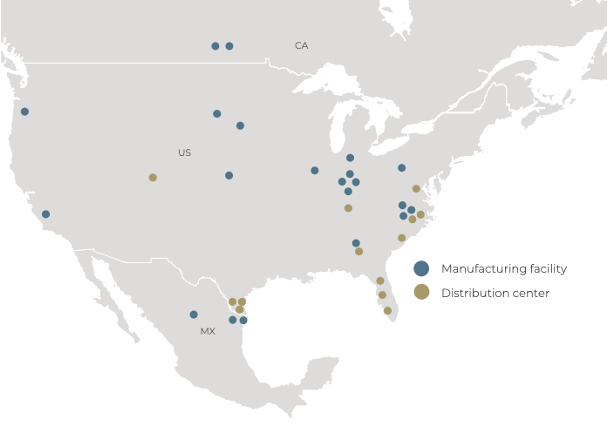

MBC manufactures the majority of its products but utilizes third parties for some items. They have 23 manufacturing facilities and 25 distribution centers across the US, Canada, and Mexico.

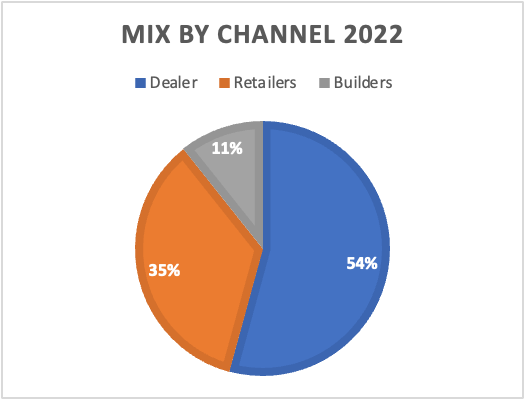

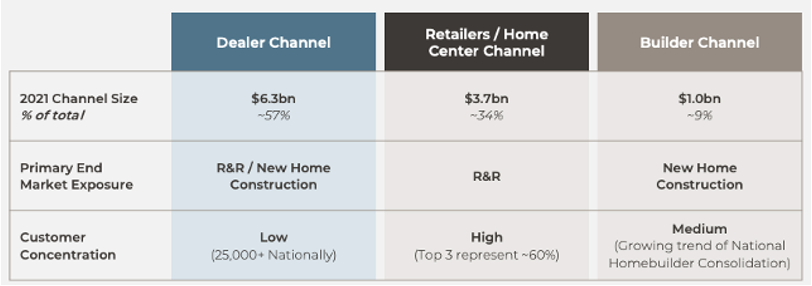

The company has the largest distribution network in North America with 4,500 across three channels: Dealers, Retailers, and Builders. They have a high degree of customer concentration coming from their largest customers with Lowes and Home Depot comprising ~37% of sales in 2022 making up most of the Retailer channel.

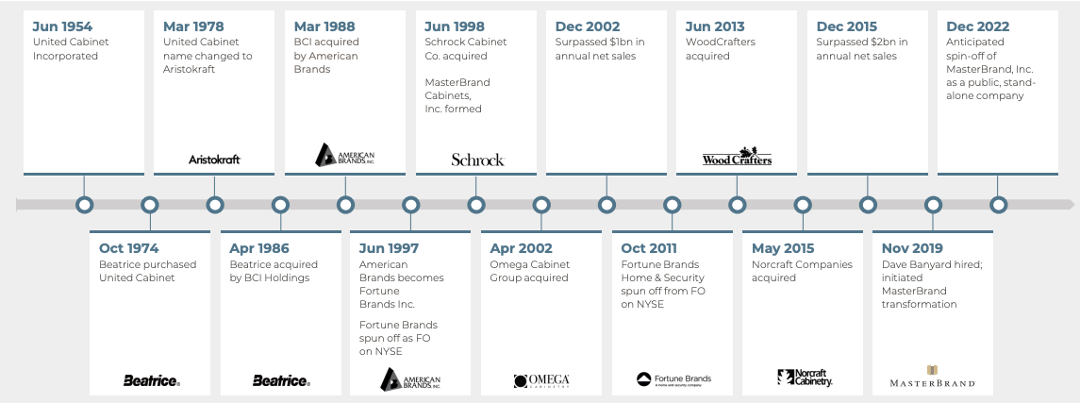

History

Masterbrand was founded 70 years ago in 1954 under the name United Cabinet. In December 2022 Masterbrand was spun out of Fortune Brands with the issuance of 128m shares where Fortune Brand shareholders receive one share of MBC stock.

Most of the company’s growth has been fuelled through M&A over the last two decades. The last 5 years have been characterized by a shift in focus towards integration and operational efficiency.

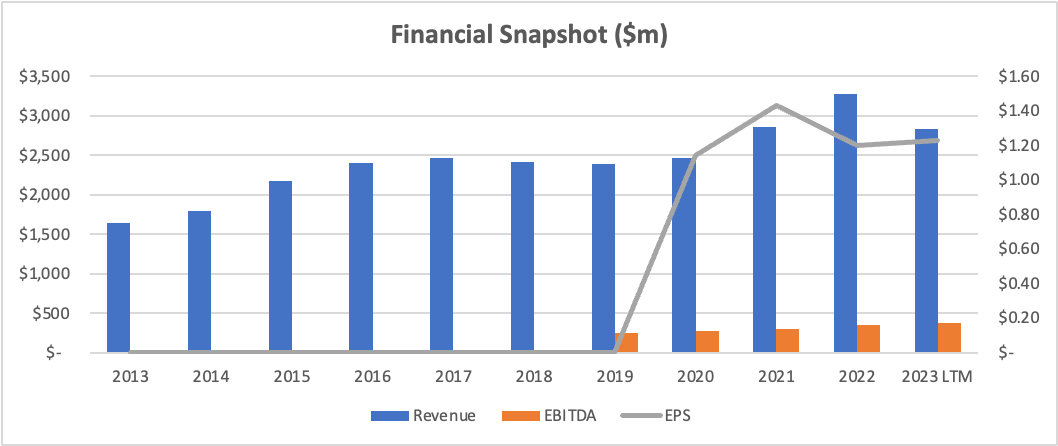

Financials

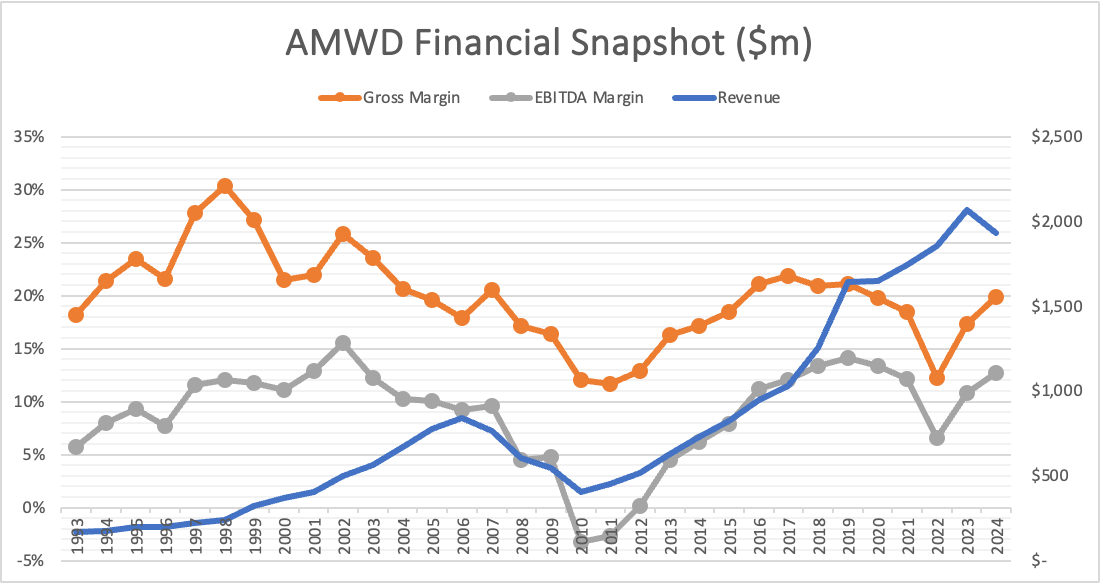

Unfortunately, we have a limited track record for MBC as a standalone company. We can see historical sales data in Fortune Brands’ financials but visibility into margins is limited.

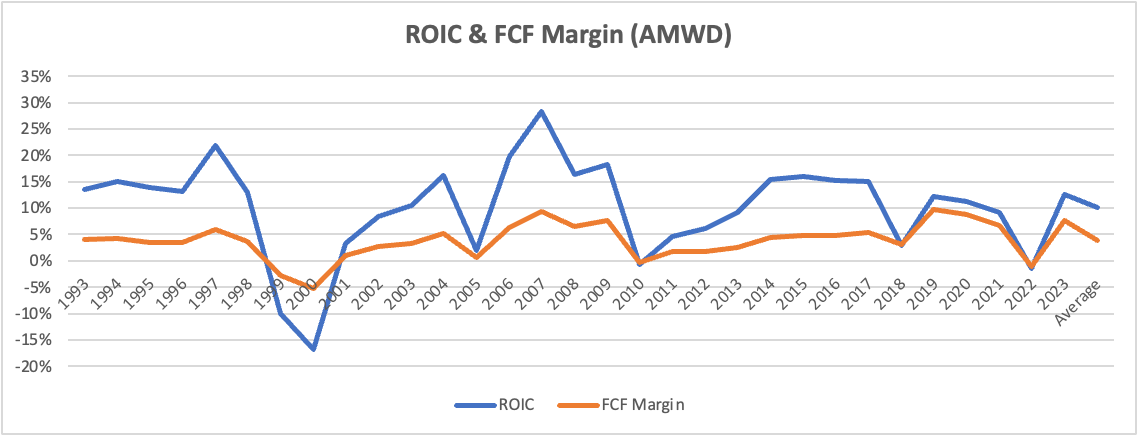

I have looked to their largest competitor, American Woodmark (AMWD), for insight. Their financials are available from 1993 onwards.

Growth has slowed over the decades and organic growth will be even lower.

Unsurprisingly, this is not a high-margin business. Cabinets are cyclical consumer products in a mature market with relatively low barriers to entry.

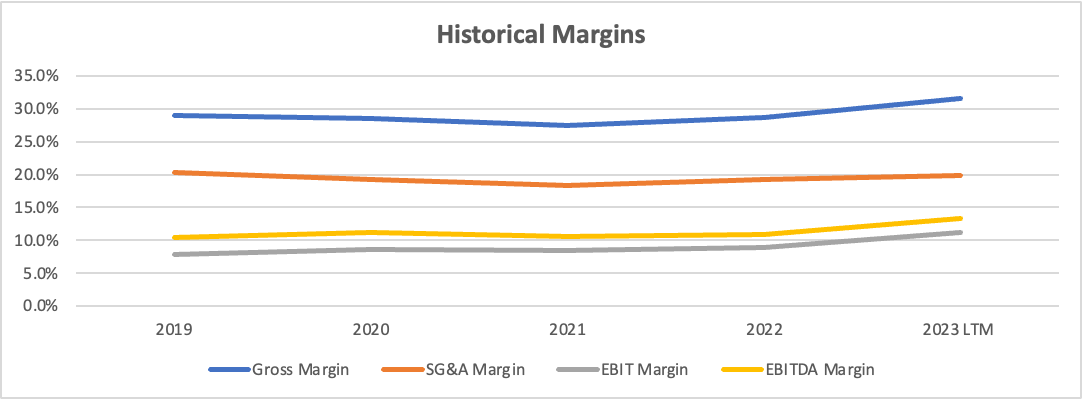

Looking at their recent operating performance. Gross margin has stepped up markedly in 2023 despite pressure on volumes. On the earnings calls they attribute this to improvements in their efficiency and rationalisation of their manufacturing network. It is hard to tell how much of this is internal improvement and what is driven by deflation in raw materials but major operating efficiencies could give us sight toward tangible margin improvements when volume returns.

Capital intensity is moderate at 1.5% of sales for MBC since 2019, the long-term run rate may be higher. American Woodmark’s CAPEX has averaged out at 3% of sales over 30 years. This needs to be taken within the context of a MSD FCF margin. If their competitor American WoodMark is anything to go by the long-run FCF margins in the industry are rather low, averaging ~4% over a 30-year history.

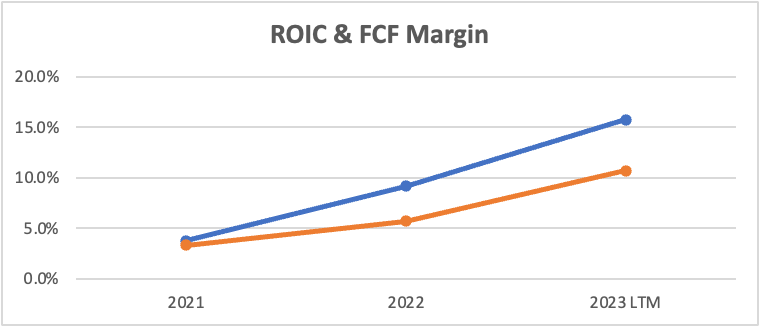

Returns on Invested Capital have been better on average at 10% but the industry’s cyclicality is very present in the chart below.

Importantly, management believes their current footprint should support planned volume growth. Once we get a return to volume growth, we should see stronger FCF and a very healthy return profile absent any material M&A or step up in CAPEX.

Balance Sheet

The balance sheet is in good order. MBC has $771m in debt (with $63.8m of leases included) and a net leverage ratio of 1.6x. The loan is partially amortizing requiring cash payments in the region of $37.5m for the next 4 years.

Recent Performance

You can read the quarterly commentary if you are interested but I will summarise the key points here:

COVID was a boon for volumes as home improvement became a key avenue for consumer spending but, volumes began to recede in 2023 and they guided industry volumes to be down LDD at their Investor Day in December 2022. The offset to this will be price realization. The company is still working through housing starts from the prior year but remodel was weak as consumers put off discretionary repairs. Unsurprisingly mix shift was also bifurcated with some consumers trading down whilst the high end remained more resilient.

Gross margins improved through most of 2023 from ~28.5% to the low 30% range over the coming quarters with management citing operational improvements. It is hard to parse out how much of this is simply moderating raw material costs or tangible operating improvements that we can get excited about.

2022

· Sales increased 14.7% to $3,275 on the back of 15.7% price growth and 1.5% volume declining 1.5%. Market conditions however have deteriorated and they expected their end-markets to be down HSD at investor day but now expect LDD declines. They will benefit from continued price annualization in 2023 but trade-downs will offset this partially.

· Backlog was down $200m yoy and is now in line with historical averages.

· Gross margin was up 120bps to 28.5% and adj EBITDA margin expanded 150bps to 12.6%. They guided to FY23 EBITDA margins of ~11-12%.

· One-time items: An asset impairment on tradenames of $46m weighed on GAAP EPS, this was following a relocation of a manufacturing site and weaker sales at another location. Restructuring charges of $25m were also recognized due to the closure of certain manufacturing facilities and we saw $15.4m in separation costs.

1Q23

· Sales declined 12.9% to $676.7m due to lower volumes that were partially offset by higher ASP. The Builders channel performed well whilst retail was slower due to excess channel inventory. Dealers were steady over the last three quarters facing difficult comps. Starts are beginning to pick up but are still below completions so the market overall will be shrinking, and repair and remodel is facing a more stretched consumer.

· Gross margin was up 300bps to 30.2% on the back of higher ASP and savings from a continuous improvement plan, in 2022 they took three facilities offline. This flowed through into a 160bps increase in EBITDA margin to 12%.

· We got our first indication of a capital allocation agenda with continued internal investments through the year, guiding to ~$50-$60m in CAPEX, share buybacks that will ‘at least’ offset SBC and they are in the early stages of developing an M&A pipeline.

2Q23

· Sales declined 18.8% to $695.1m on lower volumes that were partially offset by higher ASP annualizing price taken last year. Getting more granular on price, they saw trade-downs and some of their larger customers have index-linked pricing which will be a moderate headwind to ASP as raws come down. Repair and remodel were more dynamic with consumers taking longer whilst retail was in line.

· Gross margins were up 480bps to 34%, primarily due to strong operating performance and their rationalized footprint. EBITDA margin was 15.3%, up 280bps when adjusting for restructuring, separation payments, and environment. It is impressive to see this margin performance on such a drastic sales decline.

· Outlook for FY EBITDA was raised by $25m at the midpoint to $345 - $365 with a FY margin of 12.5% - 13%.

3Q23

· Sales were $677m, down 21% yoy with a greater than anticipated 3% headwind from trade downs. They are still annualizing price taken in the back half of last year but mix shift had a negative impact.

· By end markets: Single-family new constructions were flat yoy. Repair and Remodel were tepid and down more than expected as consumers rationalized spend. The retailers are in the final stages of destocking and performance is tracking better in higher/ lower end at dealers. A classic recession squeeze in the middle. Canada is very weak.

· Gross margin increased 420bps 35.1%, they were encouraged by the continued execution on supply chain and productivity. Adj EBITDA margin increased 153bps to 16.2%.

· CAPEX goals for the FY are $50m and net leverage was ~1.5x. The company bought back $11.5m shares and there is $35m remaining under authorization.

· EBITDA guidance for the FY was raised again to $370 - $380m with an adjusted margin of 13.5-14%.

The Market & Competiton

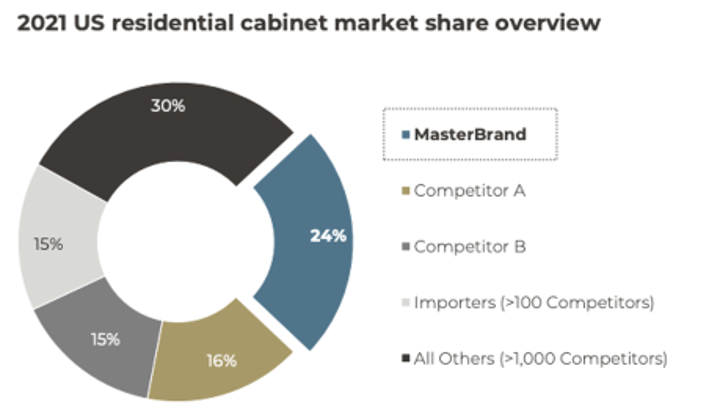

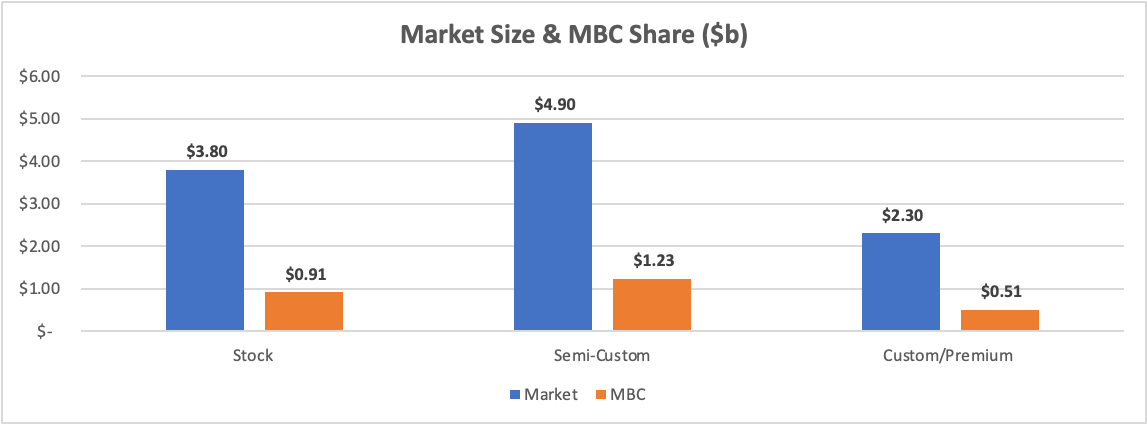

The North American cabinet market was ~$11b in 2021 and Masterbrand has ~24% share spread evenly across the three major price tiers. MasterBrand is ~50% bigger than their next two competitors (individually) who have 16% and 15% share respectively. The remainder of the market remains very fragmented with 100+ importers garnering 15% share and over 1000 independents occupying the remaining 30% of the market.

Whilst cabinets could be classed as an essential good, they remain a largely discretionary purchase in my eyes. There will always be an undercurrent of replacement demand but this should be cyclical too. A cabinet will be replaced to ‘refresh the style of a kitchen’ rather than when they are broken. So yes, we have a huge base of cabinets out there that will come up for replacement, but both New Build and Repair & Remodel will be inherently cyclical with some nuance as always.

MBC over-index in the highly fragmented dealer channel which likely conferrs some level of pricing power.

This can be seen when you look at the mix and subsequent margin difference between MasterBrand and their nearest public competitor American WoodMark (AMWD).

AMWD cites that ~60% of their offering is catered towards value, which would align with their channel mix. All this boils down to lower gross margins but relatively similar EBITDA margins. Servicing one or two large customers (Home Depot/Lowes) will come with some price concessions but likely result in operating efficiencies. The fragmented dealer market will have less influence on pricing but undoubtedly cost more the service. The other point of nuance is that the higher end of the market where MBC plays will require more SKUs to meet diverse tastes adding more complexity.

The other key competitor is Cabinetworks Group. A collection of 15 brands currently operating under Platinum Equity after a nearly 10-year stint under American Industrial. They have ~8k employees and 17 manufacturing / assembly facilities across the US. They are private and to date, I have found very little information about their operations.

Market Growth

I thought it might be useful to take some input from AMWD’s long public history. I will caveat that a portion of this growth is inorganic.

Underlying demand should roughly track population growth + inflation, approximating GDP.

Conclusion

Ultimately, this is an incredibly competitive industry that competes on quality and price.

MBC has the most extensive dealer network at 4,500 vs 1,500 for AMWD. This is hard to replicate and perhaps there isn’t even room for two large players in this market. American WoodMark describes ‘the dealer network as the largest in the nation by volume and one that rewards service levels’. You can see how a good operator could generate a degree of customer loyalty after many years of good operation. That being said, there are lots of choices in the market, and switching costs for dealers are low.

As the largest player in the market, they will benefit from some economies of scale, but these likely diminish after a certain threshold. Just look at AMWD, they are ~2/3 the size and have similar operating margins. MBC CEO, Dave Banyard pointed out that cabinets are local marekts. This results from the voluminous nature of shipping resulting in regional economies of scale, therefore the incremental benefit for a national player would be marginal. This means MBC can come up against formidable local competition in each region. The only advantages a national player has are incremental leverage on general corporate and design costs and better access to capital.

MasterBrand has exposure to the custom/premium end of the market, where trends usually emanate from. This may give them a better read on where the styles are going and allow them to better anticipate this vs competitors.

MBC are an important part of this market, but how strong is their competitive position? I will put it this way, if they took price aggressively above competitors or suffered widespread quality issues I think you would see share loss rather quickly.

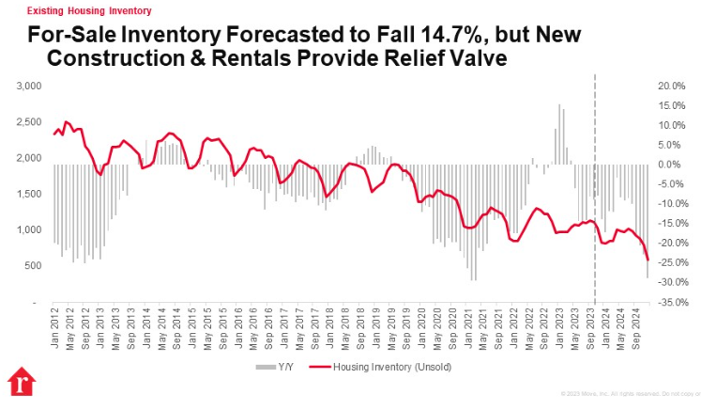

The US housing Market

I think it is important to give a lay of the land here as the US housing market is the core driver of this business. This data has mostly come from Voss Capital, who published a reverting six-part series on the US housing market.

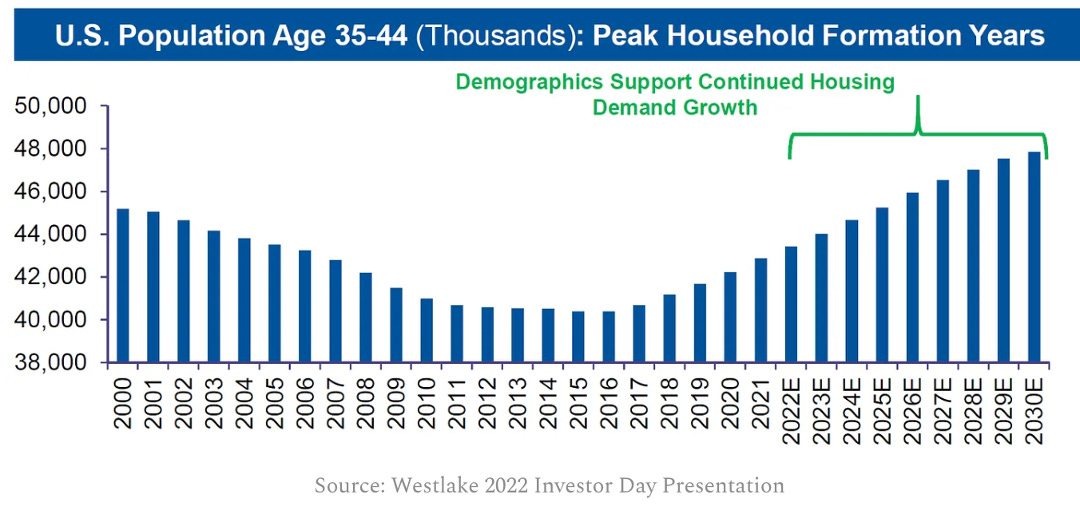

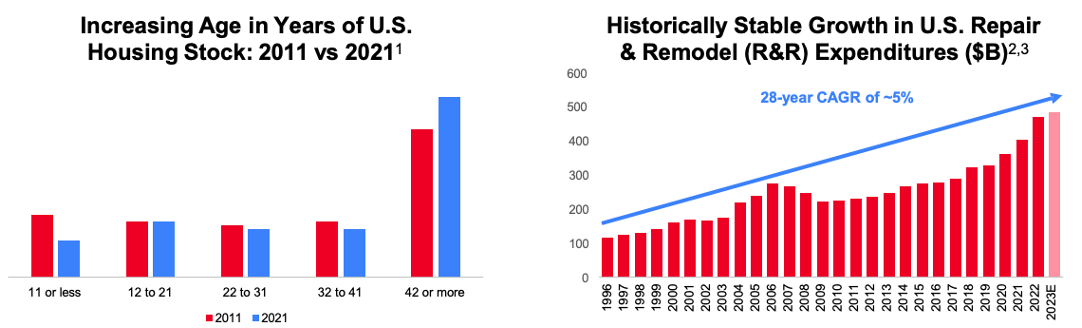

MBC management quoted a ~3m deficit in built homes (at the time of their investor day in 2022) and the average home is now 39 years old. A key driver of remodel activity. When a kitchen is redone, ~95% refresh the cabinets.

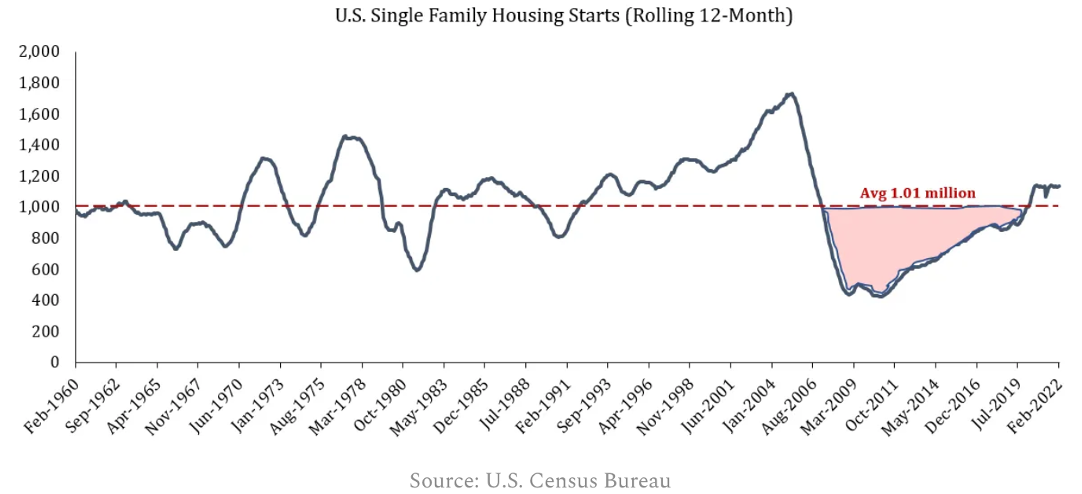

Structurally underbuilt. On average the US built 1 million homes every year since 1960 but post the GFC, between 2006 and 2019 construction was far below this level. Bear in mind, that ~0.25% of housing stock (`350k homes) is demolished every year and needs to be replaced. Couple with this underlying population growth which is 0.60% a year between 2010 and 2022.

What happened?

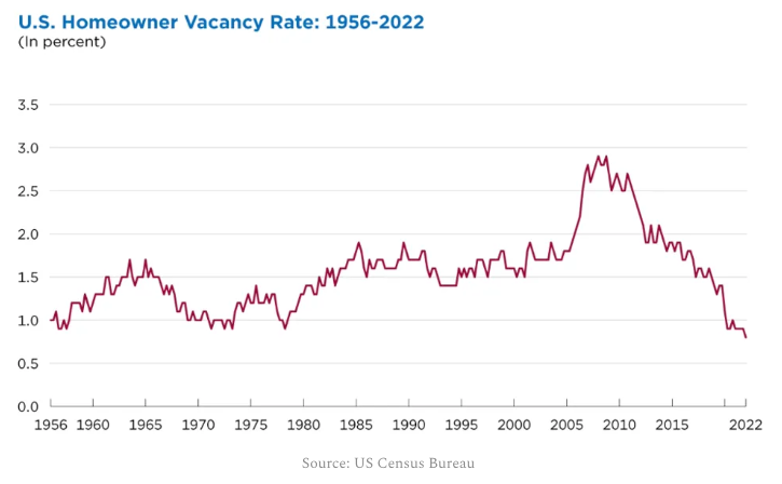

Excess inventory and weak post-crash demand. We had 38 million rental units on the market in 2009, a glut in housing supply resulting in all-time-high in vacancy rates.

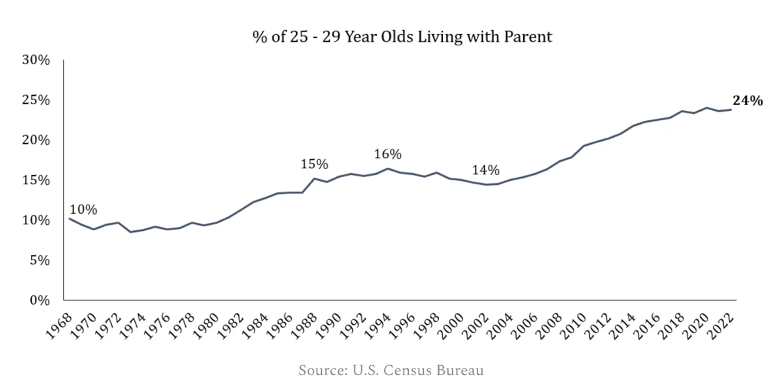

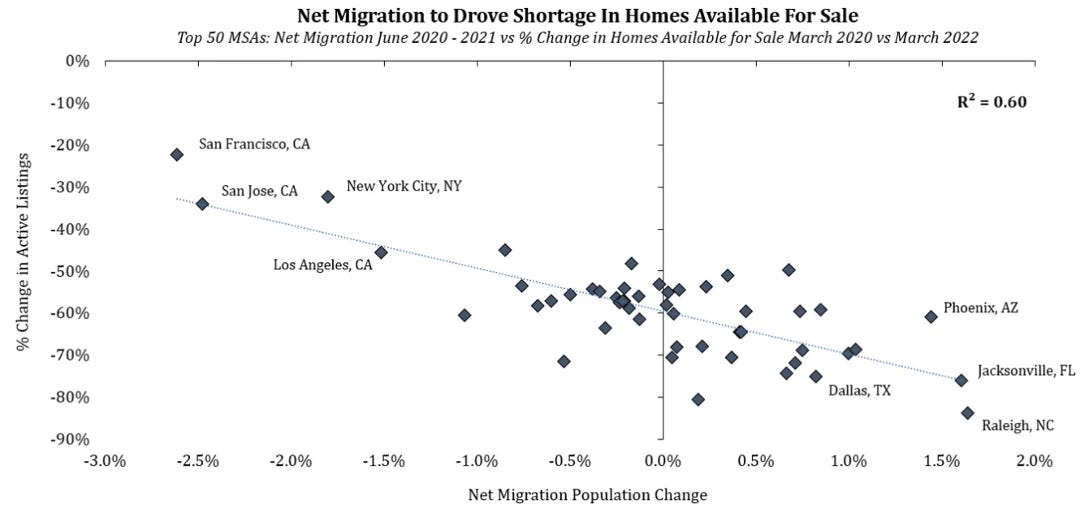

The proportion of the population aged 25-29 living at home with parents went from 14% to 19.7% between the early 2000s and 2022. An incremental 1.34m people who would have otherwise formed a household or occupied an additional unit. Has Gen-Z been saving up money living at home creating pent-up demand for new housing? Some of this pent-up demand was released during COVID and there was not a single MSA in the top 75 that didn’t have a 40% reduction in available inventory compared to the 2016-19 average (As of March 2022).

Looking Forward

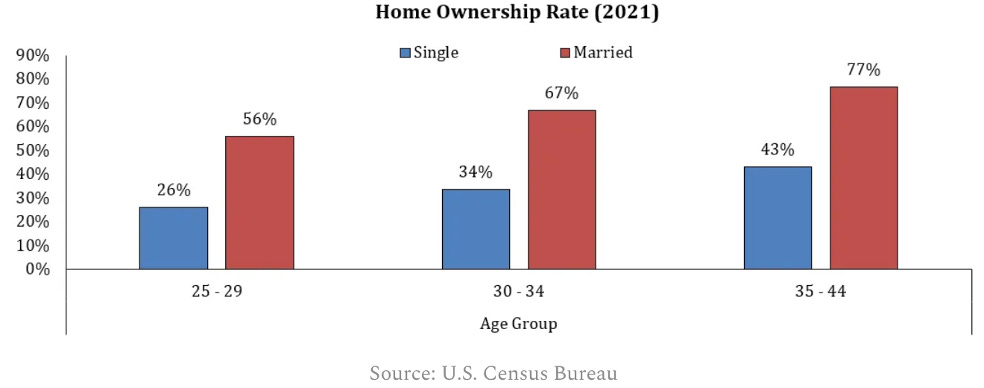

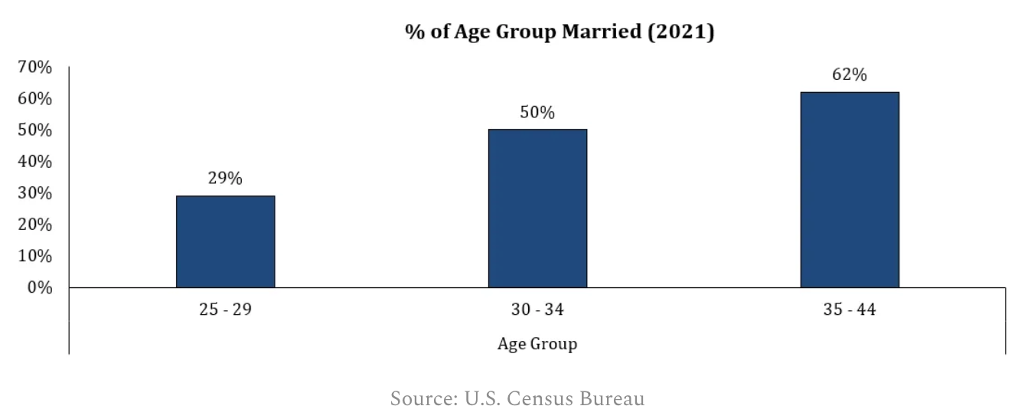

Behavior changes markedly when people turn 30. The percentage living with their parents in the 25-29 cohort drops from 24% to 14% for those between 30-34. Folks also tend to get married in their 30s, this is another key catalyst for household formation.

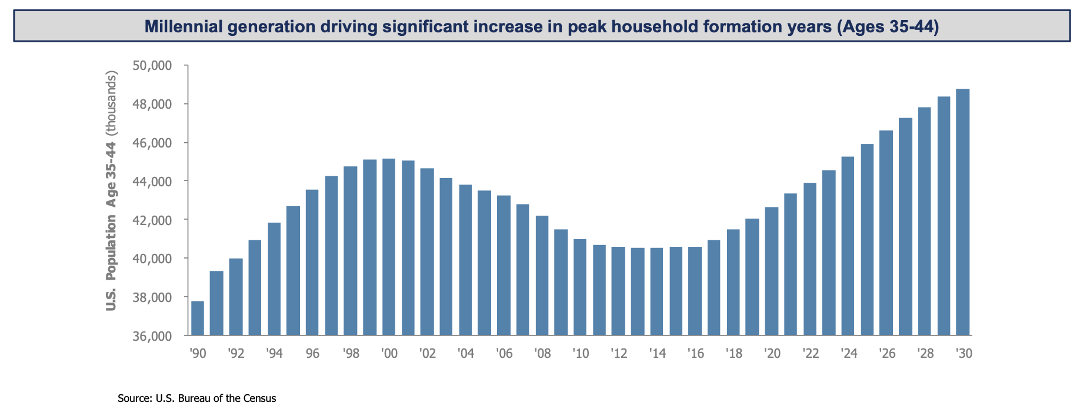

The number of people turning 30 should be a tailwind for housing over the coming years.

The above all speaks to single-family homes, thankfully multi-family units still have kitchens.

Location, location, location. Migration matters. I think it is important to address the migratory impacts on housing demand, we cannot just look at this on an aggregate basis. As the gentleman at Voss Capital so aptly put it ‘If there are 50 people and 50 units in California and Florida respectively, we have equilibrium. But when 10 people from California move to Texas, we have a need for more housing’. The migration to the sunbelt has been fuelling housing-related demand in that region for decades.

The bottom line, there should be a demographics should support housing demand for much of the next decade.

The other key factor is the age of the housing base, with refurbishments providing a solid 5% 28-year CAGR in Repair and Remodel.

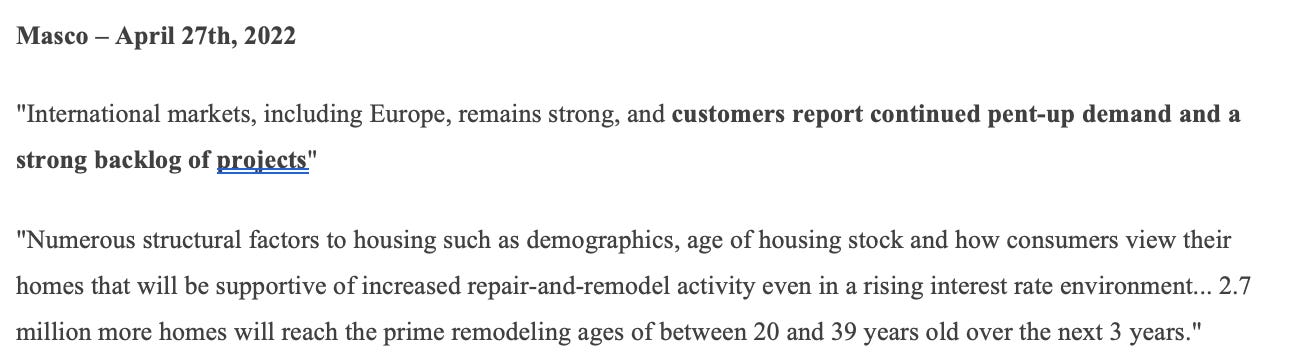

The quote from Masco succinctly sums up the favorable dynamics.

What matters near term?

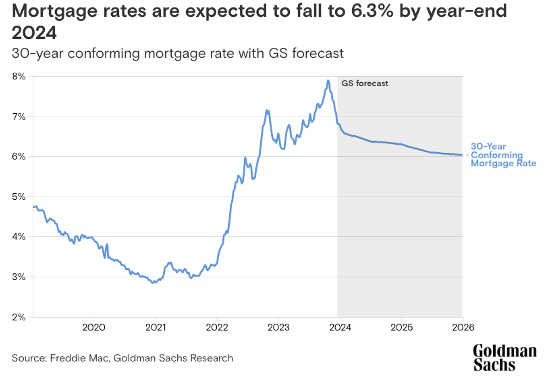

So, you have the long-term thesis above but what matters for 2024/5? Falling and importantly, stabilizing interest rates should coax some buyers back into the market.

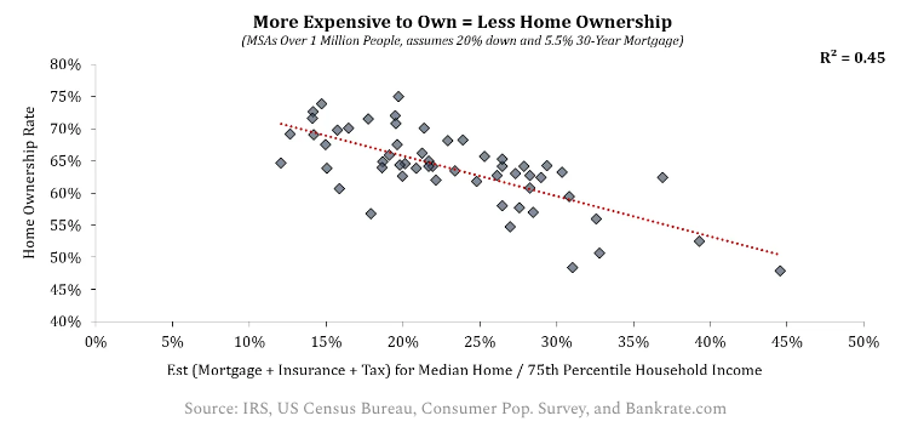

We are still in a structurally undersupplied paradigm; this is favorable for house prices but poor affordability may crimp demand. Has there been a structural shift in affordability? Will we lower levels of home ownership and more shared living in the future because people cannot afford to buy a home?

The offset for MBC to poor affordability is an increased incentive to improve the home you are in, and spend the savings you had for a move on a new kitchen.

Recent Initiatives

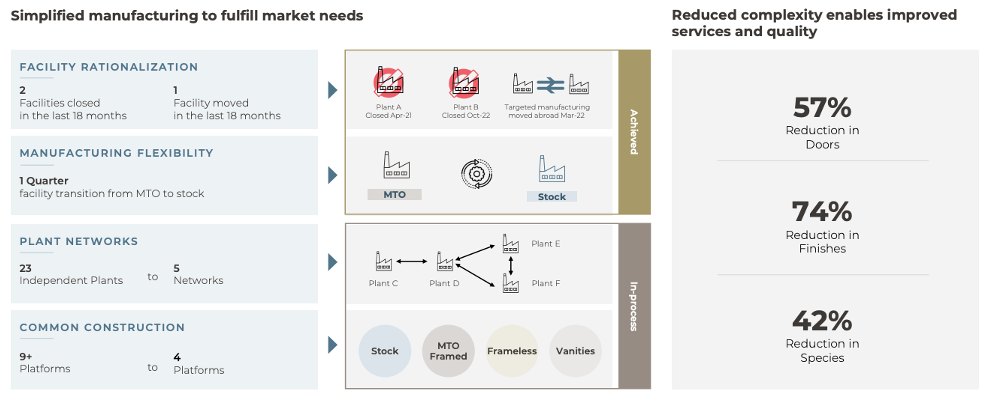

Masterbrand has made meaningful strides towards simplifying their manufacturing and now as a standalone company with a fresh management team, they have more leeway to enact change.

Align to Grow

MBC is converging its manufacturing to common platforms, like what the auto industry does to generate greater flexibility. As you can probably imagine, there are a wide variety of SKUs encompassing all sorts of styles and sizes to fit the huge number of different kitchens out there.

You can see in the chart below, that the changes have been very drastic and stand to greatly improve the simplicity of their operation. There is always a risk that the reduction in SKU could cause MBC to lose some customers at the margin, but they have noted the bulk of elimination was nearly identical to other existing products.

MBC grew through acquisitions and has many disparate operations that are typically a single brand with deep local recognition. This means that in order react to shifts in demand for any brand, that facility would need to expand in an upturn, and is often left grossly underutilized in a downturn.

In the new model, they operate networks of brands across many manufacturing plants, allowing them to shift volumes more effectively depending on the market and better handle downturns. They know this is a cyclical business and want to manage this more effectively. This also de-risks against weather events (moved production of the brand in 2022 after a tornado).

Lead through Lean

The company runs monthly Kaizen events across the company, where employees get together to bring suggestions to the table and solve problems that affect them directly.

This is a great platform for organic problem-solving, it fosters a greater culture of ownership where employees feel they have a say, and it allows strategically minded talent to get recognized and promoted. Some of the greatest companies in the world promote from within, eg; Sherwin-Williams and Costco.

Projections

Growth

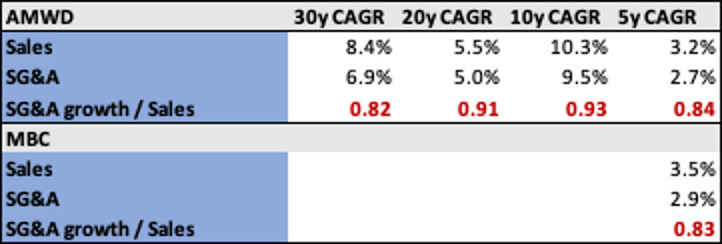

Management set out organic growth targets of 4-6%. One point above-market growth of 3-5% at the midpoint and in line with their long-run CAGR of 6.3% 15y CAGR and 4.7% 10y CAGR, although this was only partly organic. This compares to a long-term forecast of 4-5% from their competitor, American WoodMark.

We have three components of growth:

· Repair & Remodel – This has compounded at a 28-year CAGR of 5%, outside of the GFC the largest decline in R&R demand was -2.3% in 2002. Demand in any given year will be dictated by the strength of the economy. I assume 2024 is a transition year for R&R as the economy stabilizes before marching onward in 2025.

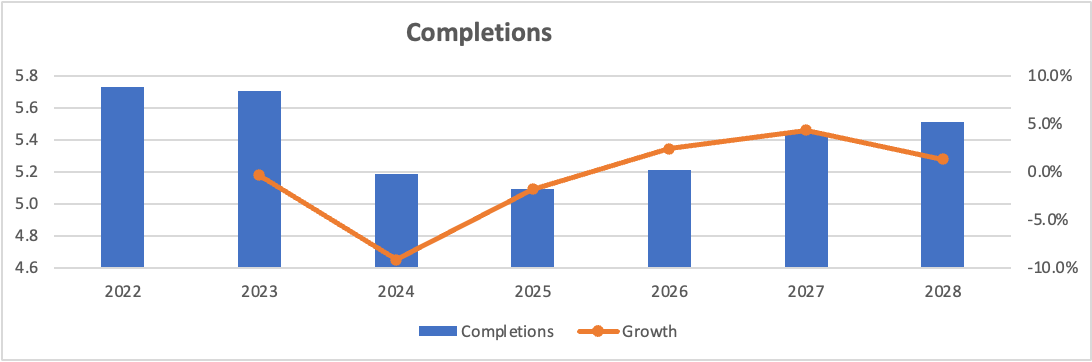

· New Starts –I pulled a forecast from Y-charts for housing starts and run completions at a 2-quarter lag. This forecast has completions down nearly 9% in 2024 digesting the lower starts in 2023 before finally returning to growth in 2026. This matches somewhat with management’s commentary of flat new builds in 2023.

· Price – This has been a huge driver of market growth recently, likely far above the historical run rate. MBC has not raised prices in 2023 and negative mix has weighed on ASP YTD. I don’t expect much direct price gains in the near term as a weaker market digests what was taken in the COVID years. In a better economic climate, moderate pricing should return and mix should be a tailwind.

Will the dip in completions above result in deflation? This is always a risk. Price is an important factor for customers and the high degree of fragmentation in the market means price discipline could be wishful.

Management said they will be more nimble than in the past and have fuel charges built into their pricing. As fuel comes down this will give the effect of a price decrease to customers whilst maintaining product margins. On promotions, they are experimental, before they cut prices they want to gauge if they have a demand problem or a price problem.

Margins

Management guided to long-term margin potential EBIT margin of 14-16% and 16-18% EBITDA margins.

As I noted earlier, their competitor AMWD achieved margins of ~14% in 2018 giving us a good context for this goal. AMWD had guided to a 13.4% EBITDA margin in 2028.

MBC has managed to grow margins against declining volumes. Either showing the effectiveness of its strategic initiatives or the benefit flowing through from moderating raw materials. They called out they are the 4th – 5th inning of these initiatives with some improvements still to come. To date, they have standardized the lower end of the market but still need to tackle the higher end which is characterized by much greater choice and a more demanding consumer. Their mindset is that the consumer wants choice, not complexity.

Another interesting call out by management was that they believe 75% of their SG&A is variable, which would allow them to manage the cyclicality in demand. Their performance so far in 2023 would attest to this.

Looking back, these businesses have been able to generate modest operating leverage over the long run. Please note that the 10y CAGR for AMWD is skewed by a large acquisition which generated some operating inefficiency.

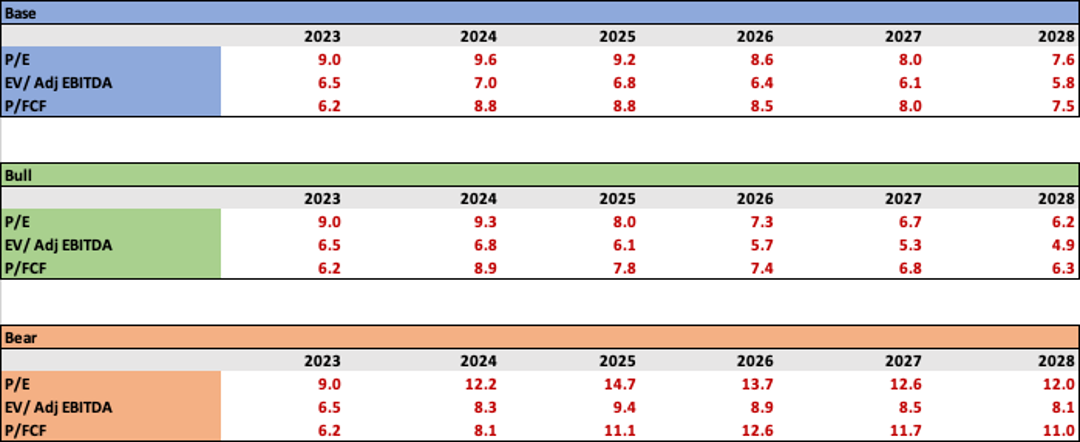

The Model

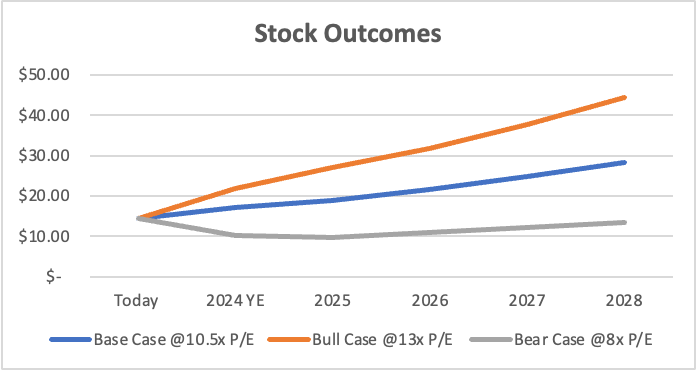

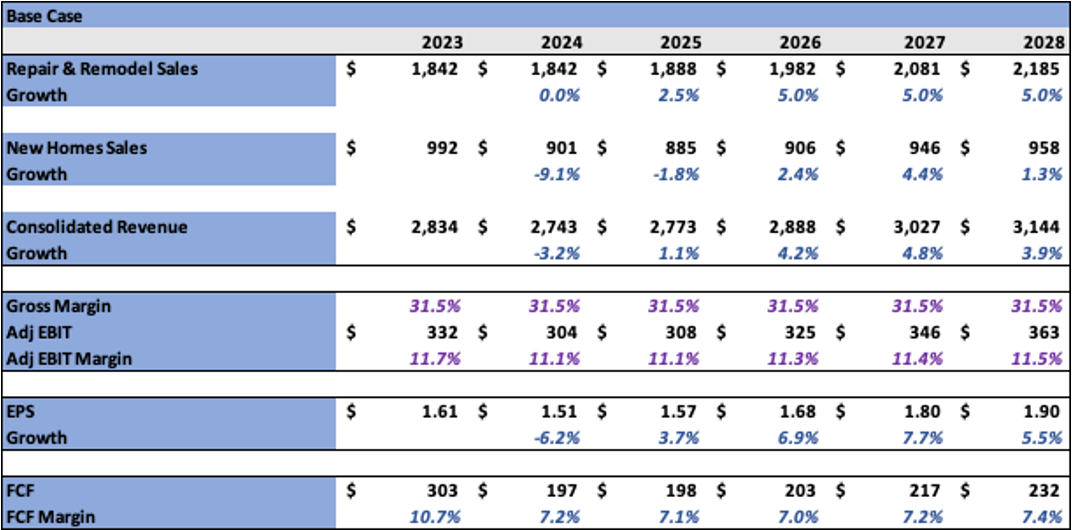

Base Case

I think R&R will pause in 2024

I have run New Builds off a Y-Charts forecast of housing starts

Gross margin is retained, and we see modest operating leverage in line with historical averages.

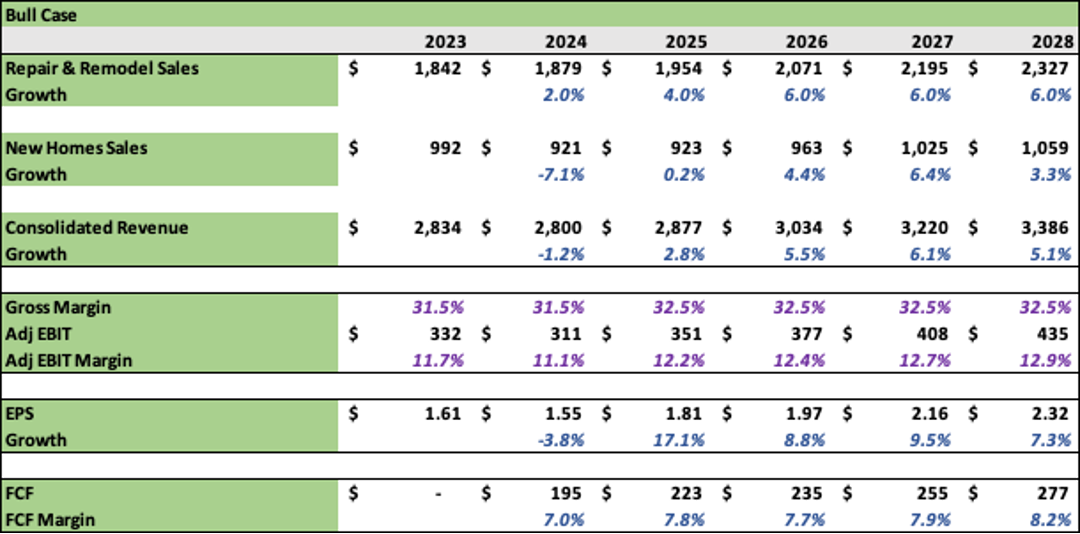

Bull Case

R&R is stronger, buoyed by the wealth effect and stronger housing market / economy.

Housing starts surprise to the upside resulting in a stronger end to 2024 and a faster return to growth.

I also give management more gross margin for future initiatives/ more favorable mix and stronger operating leverage.

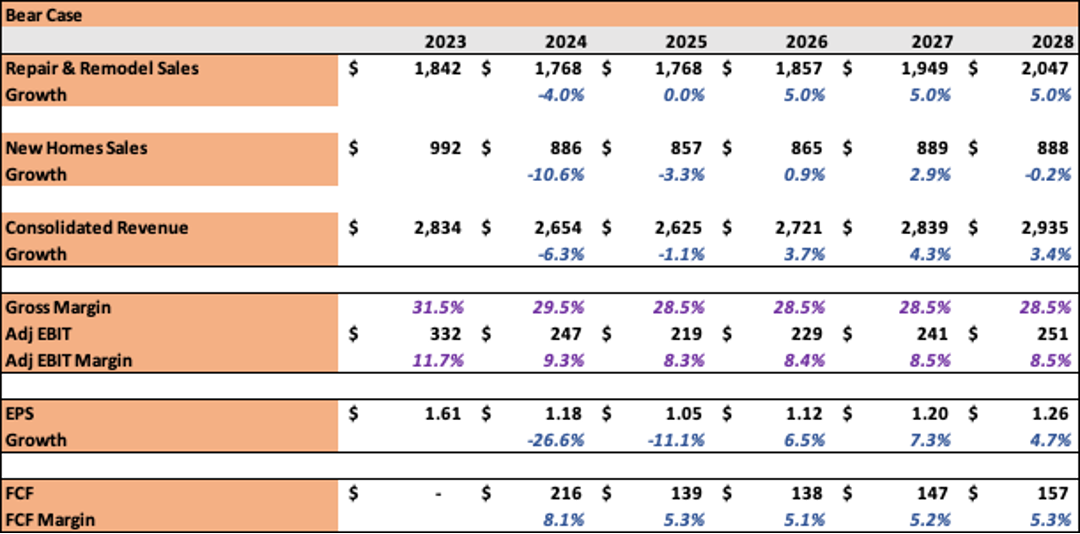

Bear Case

This is perhaps the most important picture to paint.

I worry greatly that we have seen a pull-forward in R&R demand during COVID. I don’t have this market returning to growth until 2026.

In a weaker demand environment, pricing could also come under pressure.

Margins revert and the gains made were more transitory than structural.

Capital Allocation

Management has been very proactive about paying down debt and is now at a comfortable leverage ratio. Going forward we should see more internal investment, share buybacks, and M&A.

Companies with a low P/E and a HSD FCF margin have a potent ability to juice EPS growth with buybacks. See the model below. This also has the potential to smooth earnings volatility in a downturn.

Capital allocation is so incredibly important for companies in cyclical industries. If a business can reduce their capital base this allows us to arrive at some level of compounding over time, arriving at a higher mid-cycle price without growing the business.

M&A is another priority. Looking at some old deals to gauge the level of financial arbitrage.

· AMWD: 2017 $1.075b acquisition of RSI for 8.9x pro-forma EBITDA

· FBIN: 2013 $300m acquisition of WoodCrafters Home Products

· Cabinet company for sale this $1.8m revenue, $723k EBITDA (39% margin) business is up for sale at 3.46x EBITDA and this is a high margin. This gives us some indication of the financial arbitrage MBC could achieve through.

· MBC Omega Cabinets 2002 acquisition for $538m cash

· MBC Schrock Cabinets 1998 acquisition for $107m cash

· FBINs 2015acquisition of Norcraft $600m, ~1.6x sales.

Management

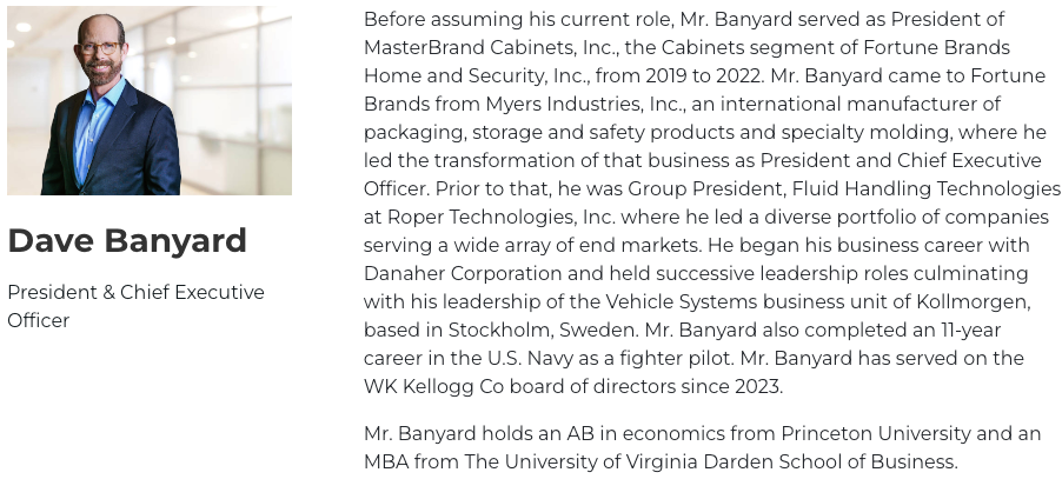

Dave has come from some of the greatest operators in the US (Danaher/ Roper) and this is evident in his language. The Danaher business system oozes from its vernacular at the 2022 Investor Day. He was also a fighter pilot which is pretty damn cool.

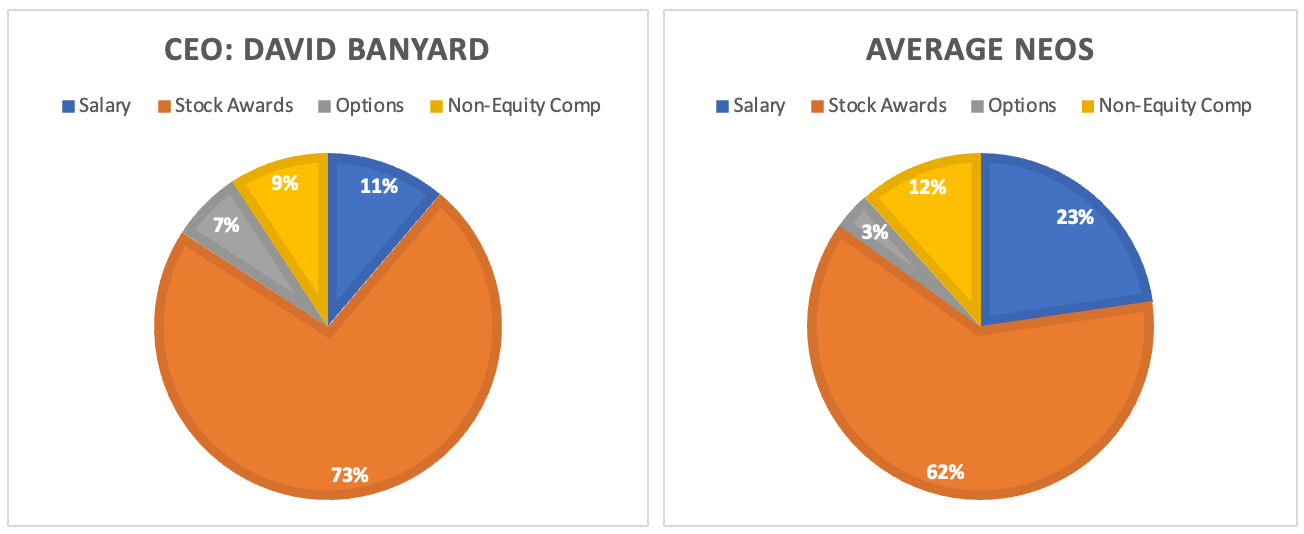

Compensation is aligned with shareholders at 70% Equity / Options for the CEO and 65%+ for other NEO’s.

Valuation

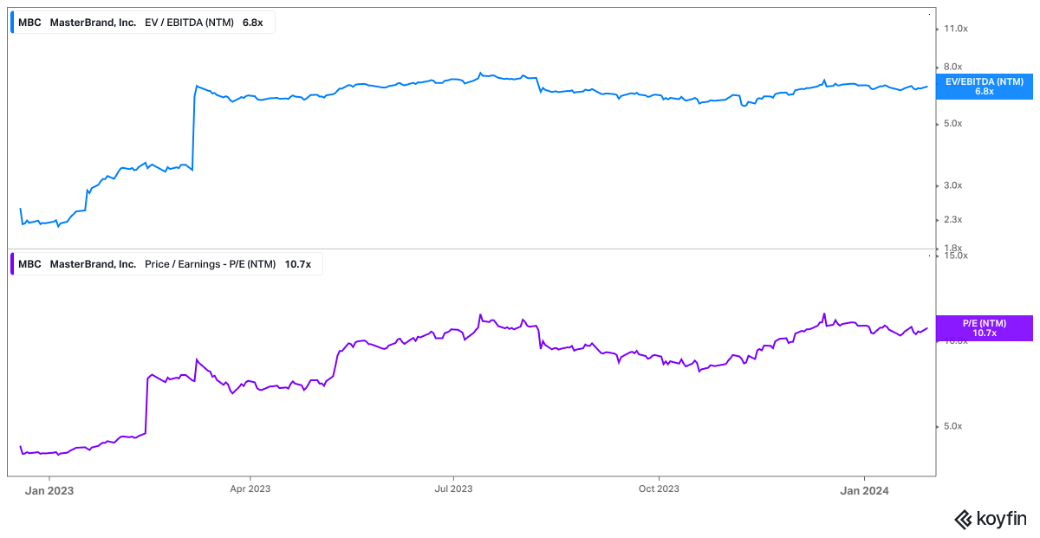

There are no two ways to slice it, MBC is cheap.

However, in my model, I do not have the company returning to meaningful earnings growth until 2025. I will caution that I may have been over-pessimistic about the pause in the R&R market and the torque remodeling could have to housing starts and lower rates.

As a cyclical, the stock should move on the back of better starts and more robust home sales. The builders rallied hard last year and investors are likely looking into other areas of the housing complex to gain cheaper exposure. A broadening of this theme should benefit MBC.

I will caveat that we are not without downside. Despite a highly flexible SG&A base if housing disappoints and we see negative operating leverage I do not see how this stock can trade at 10x. We could get a double whammy of a move to 8x and on a lower EPS number.

Similarly, a buyback-enhanced EPS growth near 20% should warrant some multiple appreciations into the low teens potentially marking significant upside.

So, the ballpark is wide, but if you believe in US housing the trajectory is likely higher over a 3-5 year horizon.

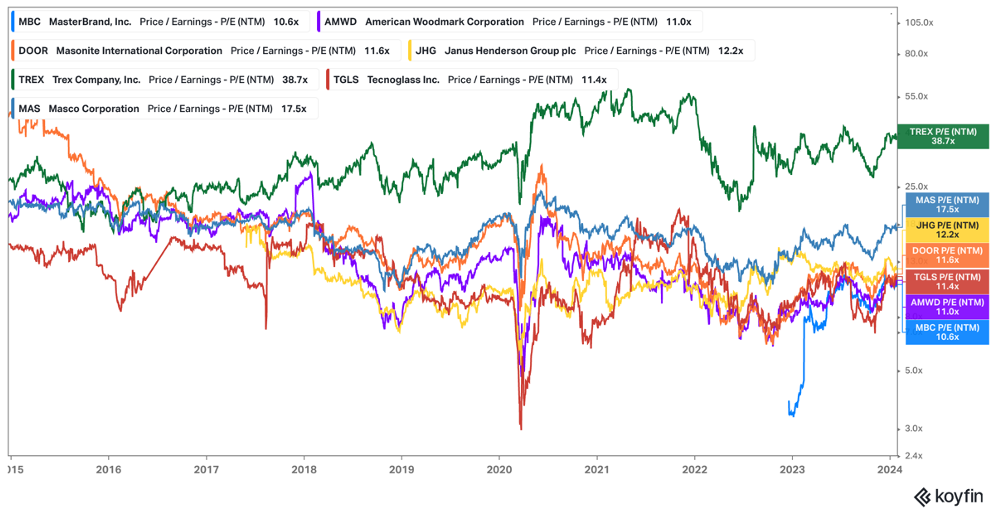

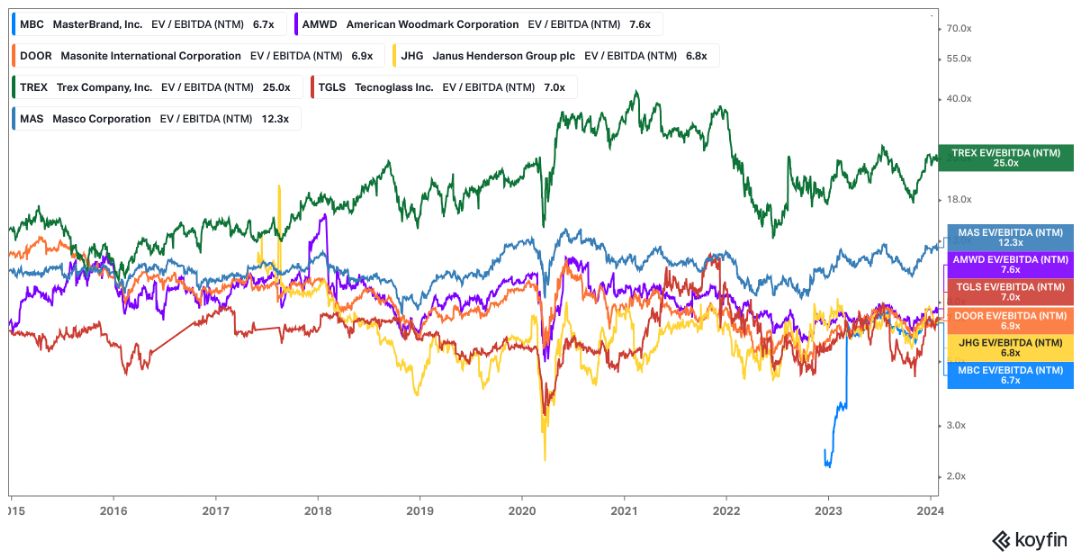

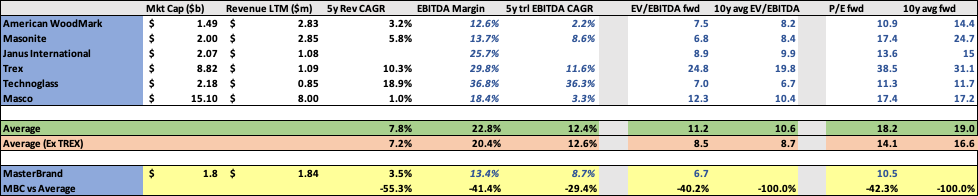

MasterBrand vs Comps

The closest comparison is AMWD. I believe MBC has a higher quality mix of business and should at least trade in line if not slightly above given the superior margin profile and faster growth.

Compared to the rest of the group, cabinets, and doors carry a lower margin and lower growth. Trex is exposed to the same cycle but is a leader in a share-gaining category. They too are an industry leader but a share gainer and category killer, probably not a fair comp.

This entire groupset should re-rate in a strong cycle and I see room for MBC to trade at a slight premium to their closest peer AMWD.